{kind=link}

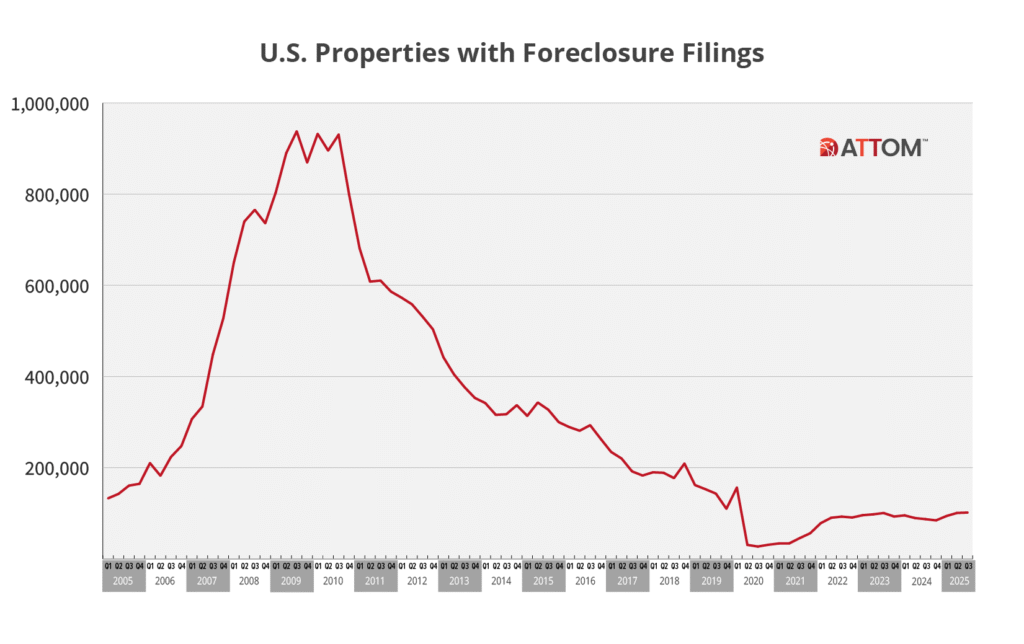

According to ATTOM’s Q3 (Third Quarter) 2025 report, foreclosure activity in the United States is on the rise, indicating increased pressure within the housing market and challenges to those desiring to keep their homes.

“In 2025, we’ve seen a consistent pattern of foreclosure activity trending higher, with both starts and completions posting year-over-year increases for consecutive quarters,” said Rob Barber, CEO at ATTOM Data Solutions, which is a leading provider of property and real estate data. “While these figures remain within a historically reasonable range, the persistence of this trend could be an early indicator of emerging borrower strain in some areas.”

The numbers tell the story. During the third quarter of 2025, a total of 101,513 U.S. properties had at least one foreclosure filing—a 17% increase from a year earlier. In September alone, 23,761 properties initiated the foreclosure process (“filings”)—up 20% year-over-year, although down approximately 2% from August.

Lenders repossessed (bank-owned) 11,723 properties in Q3 2025, an increase of 33% from the prior year.

The average time for completing a foreclosure fell to 608 days, a 25% year-over-year drop and a 6% decline from the prior quarter. Nationally, one in every 1,402 housing units had a foreclosure filing in the third quarter of 2025.

States with the worst foreclosure rates were Florida (one in every 814 housing units with a foreclosure filing); Nevada (one in every 831 housing units); South Carolina (one in every 867 housing units); Illinois (one in every 944 housing units); and Delaware (one in every 974 housing units), the report noted.

What’s driving the increase?

The pressures confronting homeowners remain severe: mortgage interest rates remain elevated; homeowners’ insurance and property taxes continue rising; major repairs and utility costs hit older homes harder;

And many purchased during the pandemic-era buying boom now face tighter budget margins. The drop in average foreclosure duration suggests that lenders and servicers are also moving more quickly into default and repossession stages.

The increases in bills came with no increase to D.C.’s Harold Richardson’s paycheck as a construction worker. His wife was a stay-at-home mom in their dream house with three small children. “I guess I was in denial about foreclosure,” he told The Final Call.

“I didn’t think it could happen to me, happened to my family, but it did. It took 18 months for me to get the message that the bank would take my house if I didn’t get my act together. I had an emotional attachment to this house and didn’t want to let it go.”

Disproportionate impact on historically underserved communities

For Black, Latino and lower-wealth households—already facing structural barriers to homeownership and building wealth—this rise in foreclosure activity is especially concerning.

Many residents in underserved neighborhoods live in older homes that require more frequent and costly repairs. With higher repair costs and fewer savings set aside, these households become more at risk.

Insurance premiums and property tax burdens often increase more quickly in urban and majority-minority communities. These additional costs cut into household budgets and add stress to mortgage payments.

Access to credit and borrower support services is disproportionately weaker in low-wealth areas. Delays in seeking assistance or navigating loss-mitigation programs can cause borrowers to fall behind sooner or have fewer options to stay afloat.

Regions with high foreclosure rates—such as Florida, South Carolina, and Nevada—include significant populations of Black, Latino, and other non-White homeowners. The failure to sustain homeownership in these areas threatens not just individual households but also entire communities’ ability to build generational wealth.

Policy implications, strategic interventions

Given the sustained increase in foreclosure filings and completions, targeted policy responses are essential. Recommendations provided by the ATTOM report include increasing culturally competent housing counseling and outreach efforts in underserved communities and educating homeowners early about options such as modification, short sale, or refinancing.

Other recommendations included providing home-repair grants or subsidies in neighborhoods where older housing dominates and repair burdens are concentrated;

Monitoring and reforming insurance- and tax-valuation practices that disproportionately raise costs in majority-minority neighborhoods and keeping home-ownership expenses manageable.

Strengthening protections and support for borrowers in the early stages of delinquency, especially in regions with high filings or short timelines to repossession, was also recommended.

“This situation is difficult at best. I wouldn’t wish it on anyone,” said Mr. Richardson about foreclosures. “Banks need to offer more options for families to save their homes.”