{kind=link}

Miles Sheridan got married and decided to sell his Prince Georges County, Maryland home. The new couple needed a bigger space. Mr. Sheridan staged his house to look appealing to potential buyers and put most of their stuff in storage. His realtor told him the house may be on the market for at least two weeks, maybe a month. It’s a seller’s market the realtor said. The first day of the sale, the Sheridan’s house was flooded with looks.

“On the third day I had an offer for more than I asked,” he told The Final Call. “I was shocked the house sold so fast. Views started on a Saturday and by Monday I had offers. I had so many people looking, they loved how it was staged. I received several really good offers. I took the highest one. It really is a sellers’ market.”

A sellers’ market is great for people selling their homes but challenging for people trying to buy. The lack of an abundant supply of new homes contributes to the growing housing crisis, especially for many Black buyers. This is despite record-low Black joblessness and a higher labor participation rate than Whites, according to the “2023 State of Housing in Black America” report recently released by the National Association of Real Estate Brokers (NAREB).

The 2023 State of Housing in Black America (SHIBA) report provides the most comprehensive annual data available on the status of Black homeownership in America. The report explained that homeownership directly impacts the overall economic growth and social equality in the United States. Increasing Black homeownership empowers and enables Black families and individuals to achieve financial stability and family economic security.

According to the report, housing demand has outpaced new home construction by roughly 100,000 units annually and has created the largest housing shortfall in nearly half a century. This has negatively affected Black homeownership. “Housing inventories must be increased across the country,” said Dr. Courtney Johnson Rose, NAREB president.

“Families can’t buy a home if they aren’t available or if the market is so tight that prices are artificially high. Clearly, there is a connection between the lack of inventory and the inability to increase Black homeownership substantially. It’s time for key components of the housing finance industry, such as Fannie Mae and Freddie Mac, to facilitate new home construction or even rehabilitation of existing homes,” added Dr. Rose.

Another challenge to home ownership is rising rents. This challenges potential home buyers by limiting their ability to save for a down payment. Rising rents, according to the report, also encourage more investors to purchase owner-occupied homes and flip them to rental stock. Couple this with rising mortgage rates, housing affordability becomes even further out of reach for many potential Black home buyers.

Zillow Research published new maps that show among Americans bearing the nation’s $600 billion total share of rental payments, Black households are particularly impacted. The Zillow maps show how census tracts with poor credit are correlated with higher rates of Black population density and places where rent is more than mortgage interest.

“Lack of credit access keeps people in a cycle of paying more in rent than they would pay each month for a mortgage on that same home,” explained Nicole Bachaud, senior economist at Zillow. “Communities of color, particularly Black families, see this play out, keeping a path to economic stability and wealth generation locked.”

According to analysts, many communities lack access to traditional and secure credit building, so even people who can afford a monthly mortgage payment may not have built up the credit necessary to qualify. Consequently, they are paying more for rent than they would if they owned a house.

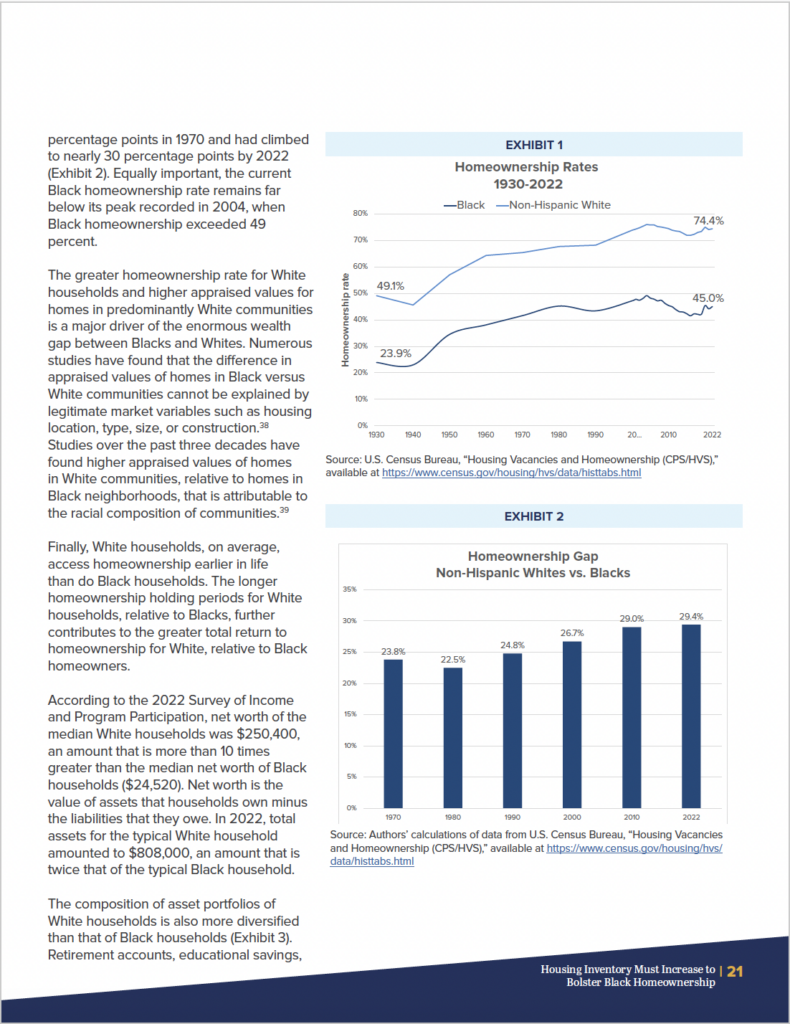

The State of Housing in Black America report found that the Black homeownership rate was 45 percent in 2022, nearly 30 percent lower than White households. This gap is wider than 50 years ago. According to the report, the Black-White wealth gap is so expansive that the 400 wealthiest Americans control the same amount of wealth as the 48 million Blacks living in the U.S.

“Narrowing the Black-White racial gaps in homeownership and wealth will require strong action at the federal level,” Dr. Rose said. “The barriers to Black homeownership date back to the early 20th Century when discriminatory housing policies such as redlining were rampant. These policies systematically excluded Blacks from acquiring loans or purchasing homes in certain areas, resulting in severe racial disparities in homeownership rates,” Dr. Rose continued.

“As a result, the wealth gap between Black and White households widened significantly over time. Today, the median net worth of White households is $250,400, compared to $24,520 for Black families. This is not societal equality,” she explained.

To address the challenges Blacks face in buying homes, NAREB launched a 100-city Black Wealth Tour, that provides financial literacy and wealth-building knowledge. There will also be a Black Development Academy in 2024 to train NAREB Members to become real estate developers.